Your insurance denial isn’t a final verdict; it’s a tactical opening move that requires a strategic legal counter-strike. You spent years paying premiums in Florida to protect your assets, only to be met with a cold rejection letter when you needed help most. It’s exhausting to feel bullied by a massive corporation while financial strain from unpaid bills piles up. If you’re facing this pressure, hiring a denied insurance claim lawyer is the first step toward leveling the playing field.

This 2026 guide shows you exactly how to challenge a denial and hold your insurer accountable for bad faith. You’ll learn about new Florida laws like HB 527, which requires a human professional to review every claim denial, and HB 459’s administrative resolution process. We’ll outline the specific deadlines your insurer must follow and explain how Charles Injury Law acts as your shield to secure full payment. From Fort Lauderdale to Palm Beach, we provide the expert representation you need to reclaim your peace of mind and secure the compensation you deserve.

Key Takeaways

- Pinpoint the exact reason for your denial to determine if the insurer is misinterpreting your policy or disputing facts.

- Master the step-by-step process of organizing your evidence and securing your full claim file from the insurance company.

- Recognize the “Delay and Pray” tactic and other lowball maneuvers insurers use to avoid paying what they owe.

- Leverage the power of Florida Statute 624.155 to pursue bad faith damages that go beyond your original policy limits.

- Learn how a denied insurance claim lawyer at Charles Injury Law acts as your shield to force a fair outcome.

Understanding Why Your Insurance Claim Was Denied in Florida

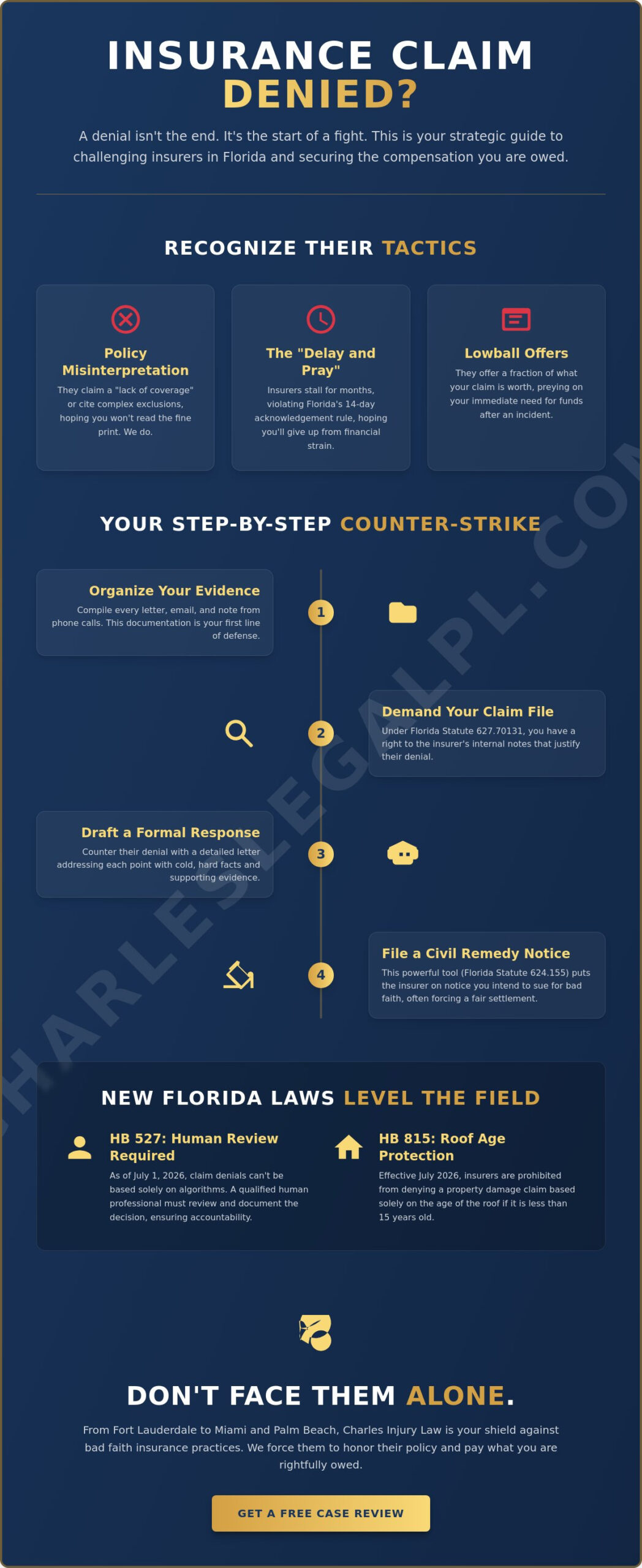

A denial letter is a punch to the gut. You opened it expecting relief but found a cold rejection instead. In Florida, insurance companies often treat your claim as a line item to be deleted. You must identify the specific reason cited in your letter immediately. This isn’t the final word. It’s a tactical move. If the insurer claims a factual dispute or a policy exclusion, don’t take their word for it. They are protecting their bottom line. Understanding the legal basis for their decision is why you need a denied insurance claim lawyer. We look past the corporate jargon to find the truth.

Insurers count on you walking away. They hope you’ll feel bullied and defeated. Don’t let them win. A denial is simply the starting point for a professional negotiation. If they refuse to pay, Charles Injury Law is ready to strike back. We analyze every sentence of your policy to find the coverage they’re trying to hide. Whether you are in Fort Lauderdale or Miami, we act as your shield against corporate greed. We ensure your voice is heard and your rights are protected.

Common Reasons for Claim Denials in Florida

Contracts in Florida are complex. Insurers often cite a “lack of coverage” to end a conversation before it starts. They might point to specific policy exclusions that you didn’t know existed. In personal injury cases, they love the “pre-existing condition” excuse. They claim your pain started years ago, not during the accident in Boca Raton or Palm Beach. Late reporting is another trap. Florida law requires insurers to acknowledge claims within 14 days, but they’ll deny you if you missed a tiny procedural deadline. They might even cite the age of your roof to deny a property claim, though HB 815 now prohibits denials based solely on roof age as of July 2026. If your denial involves auto insurance benefits, a PIP claim denial lawyer Florida residents trust can help you challenge rejections based on the 14-day rule or Emergency Medical Condition disputes.

The Role of Insurance Adjusters in the Denial Process

Adjusters don’t work for you. They work for the company. Their job is to minimize payouts. They might ignore evidence or misinterpret your statements to favor a denial. This often borders on Insurance bad faith, where the company fails to settle fairly despite clear liability. By July 1, 2026, HB 527 requires a qualified human professional to review these denials. Algorithms can’t be the sole reason for a rejection anymore. Insurers must document exactly who made the decision. Charles Injury Law steps in to hold these adjusters accountable. We level the playing field by demanding transparency and aggressive results. If the adjuster is ignoring your evidence in Fort Lauderdale, we force them to see the facts.

How to Challenge a Denied Insurance Claim: A Step-by-Step Guide

Fighting back against a massive insurance company requires a systematic counter-strike. You cannot rely on phone calls and verbal promises. If you want to win, you must build a paper trail that forces them to act. Start by organizing every piece of correspondence. Save every email, letter, and notice of denial. If an adjuster spoke to you on the phone, write down the date, time, and exactly what they said. This documentation is your first line of defense in Fort Lauderdale or Miami.

Your next move is to demand transparency. Under Florida Statute 627.70131, you have a legal right to obtain your entire claim file from the insurance company. This file contains the internal notes and logs the adjuster used to justify your denial. Once you have this, draft a formal response that addresses their specific points with cold, hard facts. If the process feels overwhelming, consulting a denied insurance claim lawyer is the most effective way to protect your interests. We know the statutes they are trying to circumvent.

If the insurer refuses to settle fairly, you may need to file a formal Civil Remedy Notice. This is a powerful tool under Florida Statute 624.155. It puts the company on notice that you are prepared to sue for bad faith. This step often forces them to reconsider their position before a lawsuit begins in Palm Beach or Boca Raton. If you are unsure whether your evidence is strong enough, speaking with a legal advocate can clarify your path forward.

Gathering Evidence to Overturn the Denial

Evidence is the only language insurance companies respect. You need a mountain of it to bury their excuses. Collect your medical records, police reports, and witness statements immediately. In many cases, you also need independent expert evaluations to counter the biased opinions of the company’s adjusters. We often utilize these experts during the Florida personal injury discovery process to prove the true extent of your damages. If your evidence is undeniable, the insurer’s path to a cheap exit is blocked.

Filing a Formal Appeal vs. Initiating a Lawsuit

You have the right to appeal a denied insurance claim through the company’s internal process. This can be faster than court, but it often feels like the fox guarding the henhouse. Internal appeals are frequently just a delay tactic. You must decide when to stop talking and start litigating. Charles Injury Law prepares every case for trial from day one. We don’t wait for the insurer to be nice. We use the threat of a jury in Florida to secure the superlative outcomes you deserve.

Common Tactics Florida Insurers Use to Avoid Paying Claims

Insurance companies aren’t your friends. They’re massive corporations focused on protecting their profits at your expense. In Florida, they use a calculated playbook to keep money in their pockets. The most common tactic is “Delay and Pray.” They wait for your bills to pile up in Fort Lauderdale or Miami. They hope you’ll get desperate enough to accept any amount they offer. If you’re feeling the squeeze of unpaid bills, then a denied insurance claim lawyer can stop the clock and force a response. We know their games and we don’t let them play with your future.

When they finally do talk, they often lead with a lowball settlement offer. They’ll frame it as a “final” or “one-time” offer. This is a lie designed to avoid a full payout. They might misrepresent your policy benefits or twist Florida state laws to make you think you’re entitled to less. If they can confuse you with complex language, then they’ve already won half the battle. They also want you to give a recorded statement immediately. They use these statements to create a “liability dispute” by taking your words out of context. Don’t let them trap you in a web of their own making.

The “Liability Dispute” Trap

Insurers love to shift blame to the victim. In car accidents, they often claim you were the one at fault. Florida follows a comparative negligence system. If they can pin 30% of the blame on you, then they save 30% on the payout. They’ll use your recorded statement to find any tiny admission of guilt to devalue your case in Palm Beach. Never give a statement without a lawyer present. Charles Injury Law acts as your shield to ensure your words aren’t twisted to benefit their bottom line. Insurers will also scrutinize every detail of your vehicle, and something as seemingly minor as non-compliant Florida tint laws violations can be weaponized to shift liability and reduce your payout.

Intentional Delays and “Missing” Documentation

Stalling is a science for these companies. They’ll ask for the same medical records three times. They’ll claim documentation is “missing” even when you have the delivery receipt from their office in Boca Raton. These intentional delays are often a precursor to a bad faith claim. If they’re playing games with your life, then it’s time to strike back with aggressive advocacy. For specific examples of these hurdles, see our Everlake Insurance denial guide. We’ve seen these patterns before. We know how to break them and secure the superlative outcomes you deserve.

The Legal Power of a Bad Faith Claim in Florida

Your insurance company has a legal duty to act in good faith toward you. If they fail to settle fairly when they could and should have, then they are violating Florida Statute 624.155. This is bad faith. It is a powerful legal weapon that turns your denied claim into a high-stakes liability for the insurer. When an insurer acts in bad faith, they are no longer just responsible for your policy limits. They may be forced to pay for all damages resulting from their conduct. A denied insurance claim lawyer uses this statute to hold massive corporations accountable for their greed in Fort Lauderdale and Miami.

Identify the red flags of bad faith immediately. If the insurer is ignoring evidence or refusing to explain a denial in Palm Beach, then you are likely a victim of corporate misconduct. To start the clock on justice, you must file a Civil Remedy Notice (CRN). This formal filing with the Florida Department of Financial Services puts the insurer on notice. It is a mandatory step before a bad faith lawsuit can proceed. If the insurer refuses to fix their mistake, then the CRN serves as the foundation for your legal strike.

Statutory vs. Common Law Bad Faith in Florida

Florida law recognizes both first-party and third-party bad faith claims. First-party claims involve your own insurer failing you. Third-party claims involve an insurer failing to settle a claim brought against you. Once the CRN is filed, the insurer has a 60-day window to “cure” the violation. If they pay the full value of the claim within this period, then the bad faith suit is usually blocked. Charles Injury Law leverages this 60-day deadline to force immediate action. We don’t let insurers hide behind bureaucratic delays in Boca Raton. We demand accountability and superlative outcomes.

Recoverable Damages in an Insurance Dispute

Winning a bad faith case means more than just getting your original claim paid. You are entitled to the full amount of the original claim plus interest from the date of the loss. If we succeed in court, then Florida law often requires the insurance company to pay your attorney fees. This shifting of legal costs removes the financial burden from your shoulders. In extreme cases involving malicious or reckless conduct, you may even recover damages for emotional distress or punitive awards. If you believe your insurer is acting in bad faith, then contact Charles Injury Law today to discuss your strategy.

Why Charles Injury Law is Your Shield Against Denied Claims

Facing a massive insurance company alone is a losing battle. These corporations have unlimited resources and legal teams designed to protect their profits at your expense. Charles Injury Law provides the aggressive representation you need to fight back in Fort Lauderdale and Miami. We act as your formidable shield. While you focus on your physical and emotional recovery, we handle the high-stakes conflict with the insurer. If you’ve been ignored or bullied, then hiring a denied insurance claim lawyer is how you reclaim your power and demand accountability.

Our firm operates on a contingency fee basis. This structure removes the financial risk from your pursuit of justice. If we do not win your case, then you do not pay us a single cent in attorney fees. This direct commitment ensures our goals are perfectly aligned with yours. We are not a detached corporate entity; we are a dedicated ally. Our team is trial-ready from the moment we take your case. We do not settle for lowball offers that fail to cover your bills. We fight for the superlative outcomes you deserve and the financial restitution you need to move forward.

Aggressive Advocacy in Boca Raton and Palm Beach

Success in South Florida courtrooms requires deep local expertise and a confrontational spirit. We know how insurers operate in Palm Beach and Boca Raton. Our team has extensive experience countering the specific legal tactics used by major insurance companies to avoid liability. We specialize in high-stakes disputes, including denials related to wrongful death and complex claims involving commercial vehicles, where working with a dedicated truck accident lawyer is essential to overcoming the corporate machine behind every carrier’s insurance defense. If an insurer thinks they can escape their obligations through complex policy language, then we prove them wrong through relentless litigation and technical mastery of Florida law.

Schedule Your Free Consultation Today

The path to financial restitution should be clear and unobstructed. You don’t have to navigate the complex world of insurance law while in pain or financial distress. Charles Injury Law is ready to review your denial and build a strategic counter-strike immediately. We provide immediate authority and ease of access for individuals who feel overwhelmed by corporate giants. Starting your case is simple and requires no upfront costs. A single phone call connects you with a protective champion who is ready to act on your behalf. Contact Charles Injury Law today for your free case evaluation.

Secure the Restitution You Deserve

An insurance denial is a tactical maneuver, not a final verdict. You now know that Florida law provides powerful tools to challenge corporate greed. From mandatory human reviews under HB 527 to bad faith litigation via Statute 624.155, the law is on your side. If an insurer refuses to pay what they owe, then a denied insurance claim lawyer is your most effective counter-strike. We dismantle their excuses and force them to respect your policy.

Charles Injury Law stands ready to act as your protective champion in Fort Lauderdale, Miami, and Boca Raton. We are trial-ready personal injury experts who refuse to settle for less. Our firm operates on a risk-free basis; if we don’t win, you don’t pay. We handle the intense legal conflict so you can focus on your recovery. Get the Aggressive Representation You Deserve; Contact Charles Injury Law Now. Your fight for justice starts with a single call; let us secure your future.

Frequently Asked Questions

Can I sue my insurance company for denying my claim in Florida?

Yes, you can sue your Insurance Company if they breach their contract or act in bad faith. Florida Statute 624.155 allows you to pursue damages when an insurer fails to settle fairly. If they are ignoring evidence or misinterpreting your policy in Miami, then a lawsuit is a necessary strike. Charles Injury Law handles these high-stakes disputes to ensure you receive superlative outcomes. We hold these corporations accountable for every cent they owe you.

How long do I have to challenge a denied insurance claim in Florida?

The statute of limitations for filing a breach of insurance contract lawsuit in Florida is five years from the date of the loss. If you are filing an internal appeal for a Marketplace health plan, then you typically have 180 days from the denial notice. Missing these deadlines can kill your case. Contact a denied insurance claim lawyer immediately to protect your rights in Fort Lauderdale and ensure your filing is on time.

What is a “Bad Faith” insurance claim under Florida law?

Bad faith is a legal concept defined under Florida Statute 624.155. It applies when an Insurance Company fails to properly investigate a claim or refuses to pay when liability is clear. If the company is putting their profits over your recovery in Palm Beach, then they are acting in bad faith. This allows you to seek damages that may exceed your original policy limits. We specialize in proving these violations in court.

Do I have to pay a lawyer upfront to fight a denied claim?

You don’t have to pay Charles Injury Law anything upfront. We work on a contingency fee basis; if we don’t win, you don’t pay. This risk-free approach ensures that every resident in Boca Raton has access to elite legal representation. We handle the costs of litigation and expert witnesses so you can focus on your physical recovery. Our firm only gets paid when we secure a successful financial recovery for you.

What should I do if the insurance company offers a lowball settlement after a denial?

Do not sign any documents or accept a “final” check without consulting a professional. These lowball offers are designed to save the Insurance Company money at your expense. If you accept a settlement too early, then you lose the right to seek more money later. A denied insurance claim lawyer analyzes these offers to ensure they cover the full extent of your damages. We negotiate aggressively to turn a low offer into a fair payout.

Can an insurance company deny a claim for a car accident that was not my fault?

Yes, insurers frequently deny claims for accidents where you were the victim. They might claim you were partially at fault under Florida’s comparative negligence rules to reduce their payout. They also use technicalities like late reporting or policy exclusions to avoid responsibility. Charles Injury Law acts as your shield in these situations to prove the truth and secure the compensation you deserve. We don’t let them shift the blame to you.

How long does an insurance company have to investigate a claim in Florida?

Under Florida Statute 627.70131, the Insurance Company must acknowledge your claim and begin an investigation within 14 days. They are required to provide a written statement of coverage within 30 days. Finally, they must pay or deny the claim within 90 days of receiving your proof of loss. If they miss these deadlines in Miami, then they may be in violation of state law. We track these dates closely to hold them to the legal standard.

What happens if my insurance company ignores my appeal?

If an Insurance Company ignores your appeal, then you should file a formal Civil Remedy Notice. This document starts a 60-day window for the insurer to fix their mistake. If they still refuse to act, then you have the foundation for a bad faith lawsuit. Charles Injury Law uses these procedural moves to force a response from stubborn insurers in Palm Beach. We don’t wait for them to be ready; we demand action immediately.

Disclaimer

The information provided on this blog is for general informational purposes only and does not constitute legal advice. Viewing this content does not create an attorney-client relationship with the firm. You should not act or rely on any information contained herein without seeking legal advice from a qualified attorney regarding your individual situation.