What if the term "no-fault" is actually a shield for insurance companies rather than a safety net for you? If you’re recovering from a crash in Fort Lauderdale or Miami, you’re likely asking, is Florida a no fault state? The answer is yes, but don’t let that label fool you into thinking you can’t hold a negligent driver accountable. We know you’re feeling the weight of rising medical costs and the anxiety of lost wages. It’s a high-stakes situation where every hour counts, and the confusion over legal terminology only adds to your distress.

This article will clear the confusion surrounding Florida’s insurance laws and show you how to secure maximum compensation. We’ll explain the strict 14-day medical treatment rule and identify when your injuries allow you to step outside the PIP system to sue for pain and suffering. If you need a relentless advocate, Steve Charles is ready to fight for your financial restitution. We will preview the essential steps to take within the two-year statute of limitations to ensure your claim isn’t just filed, but won.

Essential Insights on Florida's No-Fault Laws

- Discover why is Florida a no fault state and how this designation impacts your ability to recover costs immediately after a crash.

- Master the 14-day medical rule to ensure you don’t forfeit your mandatory $10,000 in Personal Injury Protection benefits.

- Identify the specific legal thresholds that allow you to hold negligent drivers accountable for pain and suffering in Fort Lauderdale.

- Debunk common myths that prevent accident victims from seeking full financial restitution beyond their own insurance policies.

- Learn how Steve Charles provides the aggressive advocacy needed to defeat insurance company denials and secure superlative outcomes.

Table of Contents

Understanding Florida’s No-Fault Insurance System

Florida law requires every driver to carry insurance that pays their own medical bills. This is why many people ask, is Florida a no fault state? Yes, it is. This system was designed to ensure that if you get hurt, you get paid quickly without waiting for a court to decide who was wrong. By Understanding Florida’s No-Fault Insurance System, you can see the state’s attempt to keep minor fender-benders out of the crowded courtrooms in Miami and Fort Lauderdale.

Don’t let the name confuse you. "No-fault" doesn’t mean no one is responsible. It simply means your own insurance is your first stop for medical costs. If you are sitting in gridlock in Boca Raton and someone rear-ends you, your Personal Injury Protection (PIP) coverage handles your initial doctor visits. However, the "no-fault" label only applies to bodily injury. Property damage is a different story. The person who hit you is still financially liable for the crumpled metal of your car. This distinction is critical for victims who feel stuck after a wreck.

The History and Goal of Florida’s No-Fault Laws

The Florida Legislature enacted these laws in the early 1970s. The goal was simple; reduce the massive burden on the court system. They created a trade-off for drivers. You get fast, guaranteed payments for minor injuries, but you lose the right to sue for small claims. When you ask is Florida a no fault state, you have to look at how the law has evolved. As traffic density has exploded in South Florida over the decades, this system has become a double-edged sword. It provides a baseline of support, but it often leaves victims with serious injuries under-compensated and struggling to pay bills.

How ‘No-Fault’ Affects Your Right to Recovery

Your PIP policy is your primary shield. It covers 80% of your medical bills and 60% of your lost wages, up to $10,000. But $10,000 disappears fast in a modern emergency room. If your injuries are severe, the "no-fault" rules can feel like a cage. You must act immediately to preserve your rights. The other driver’s negligence still matters if you want to recover more than just the bare minimum. Steve Charles knows how to pierce through these insurance limitations to find the accountability you deserve. If you’ve been hurt, visit our car accidents page to see how we fight for your financial restitution. We don’t let insurance companies hide behind confusing terminology while you suffer.

The Role of Personal Injury Protection (PIP) in Florida

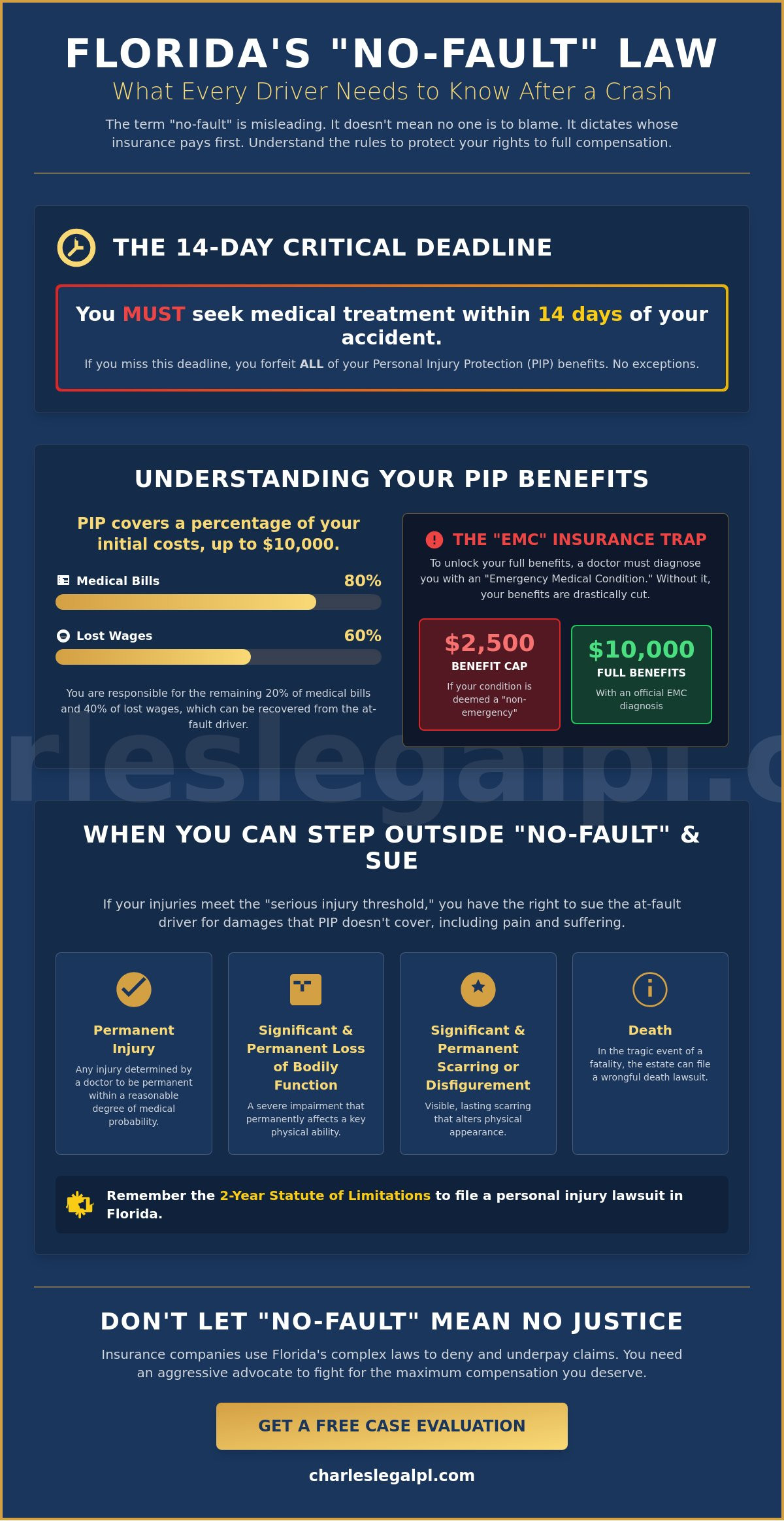

Every driver in Florida must carry at least $10,000 in Personal Injury Protection (PIP). This coverage is the cornerstone of why is Florida a no fault state. It’s designed to act as your immediate financial shield. But don’t assume the money is guaranteed just because you pay your premiums. If you don’t seek medical care within 14 days of the crash, you lose your benefits entirely. This 14-day rule is a hard deadline. Insurance companies love it when you wait because it gives them a legal reason to keep their money in their pockets.

The system is built for speed, but it often sacrifices total coverage. PIP only pays 80% of your medical bills and 60% of your lost wages. If you have $10,000 in medical costs, your insurer only pays $8,000. You are still on the hook for the rest. This gap is why understanding When You Can Sue: The Serious Injury Threshold becomes vital for victims in Miami and Fort Lauderdale. When your costs exceed these limits, you need a strategy to recover the difference.

What Does PIP Actually Cover After a Crash?

PIP medical benefits cover a wide range of treatments. This includes emergency room visits, surgeries, X-rays, and dental work. It also covers rehabilitation and prosthetic devices. If your injuries prevent you from working, disability benefits provide a lifeline. This coverage applies to lost gross income and loss of earning capacity. It even covers "replacement services" like house cleaning or childcare if your injuries prevent you from performing them. In the most tragic cases, PIP provides a $5,000 death benefit to help families in Boca Raton with funeral and burial expenses.

The Hidden Traps of PIP Insurance

The system has a massive loophole that favors insurers. To unlock the full $10,000 benefit, a licensed medical professional must diagnose you with an "Emergency Medical Condition" (EMC). If they don’t, your benefit is capped at a measly $2,500. Insurers often use this "non-emergency" designation to shortchange victims. They might also try to trick you into giving a recorded statement. One wrong word can lead to a denied insurance claim. In a serious car accident, $10,000 is gone before you even leave the hospital.

If you’re feeling overwhelmed by these complex rules, you don’t have to fight alone. Steve Charles acts as a formidable shield for his clients. He ensures that insurance companies don’t use technicalities to rob you of your recovery. If you’re struggling with an insurance company that won’t pay, reach out to us today for an aggressive advocate who knows how to win.

When You Can Sue: The Serious Injury Threshold in Florida

Many accident victims believe they are stuck with the $10,000 PIP limit. This is a dangerous misconception. While is Florida a no fault state, the law provides a specific gateway to hold negligent drivers accountable. This gateway is the "serious injury threshold." If your injuries meet the criteria under Florida Statute 627.737, you can bypass the no-fault system entirely. You can sue the at-fault party for your full medical expenses, lost wages, and non-economic damages.

Proving you meet this threshold requires more than just a doctor’s note. It requires bulletproof medical documentation. Insurance companies in Miami and Fort Lauderdale will fight to keep your case trapped in the no-fault system. They want to cap their liability at the PIP minimum. We use aggressive advocacy to prove the true extent of your suffering. If your injury is permanent, you deserve a superlative outcome that reflects your reality. Steve Charles acts as a formidable shield, ensuring that technicalities don’t block your path to justice.

Criteria for Filing a Lawsuit Against the At-Fault Driver

To step outside the no-fault limits, your injury must be severe. Florida law recognizes four specific categories that meet the threshold. First, you must prove a significant and permanent loss of an important bodily function. Second, you may show a permanent injury within a reasonable degree of medical probability. Third, significant and permanent scarring or disfigurement qualifies you for a personal injury lawsuit. Finally, cases involving wrongful death automatically bypass these restrictions. We don’t accept vague diagnoses; we demand clarity from medical experts to build your case.

Seeking Pain and Suffering Damages

PIP is designed to cover bills, not your quality of life. It provides zero compensation for pain, suffering, mental anguish, or loss of enjoyment of life. This is why meeting the serious injury threshold is so critical. Once you cross that line, you can seek full financial restitution for these non-economic losses. A reckless driver in Boca Raton should not get a free pass just because of "no-fault" labels. Steve Charles fights to expose the impact the crash has had on your daily life. If your life has been forever changed, your compensation must reflect that change. We don’t just file papers; we prepare every case for trial to maximize your recovery.

Common Misconceptions About No-Fault Laws in South Florida

Living in Miami or Fort Lauderdale means dealing with some of the most aggressive drivers in the country. When a crash occurs, the term "no-fault" is often thrown around by police and insurance adjusters. This leads to a dangerous level of complacency. While the legal answer to is Florida a no fault state is a firm "yes," the practical reality is far more complex. Victims often believe the system is designed to protect them automatically. It isn’t. It is designed to limit the financial exposure of insurance corporations.

The first major misconception is that you can never sue the other driver. If your injuries are life-altering, the no-fault rules do not apply to you. Another common trap is believing your own insurance company will "take care of you" because you weren’t at fault. Your insurer is a business. Their goal is to pay out as little as possible to protect their bottom line. Finally, many victims think they don’t need a lawyer for a simple PIP claim. This mistake often results in capped benefits and ignored medical bills that eventually end up in collections.

Debunking the ‘Immunity’ Myth

Negligent drivers are not immune from liability in Florida. If a driver’s recklessness causes a catastrophic event, they can be held accountable in court. This is especially true in complex scenarios like truck accidents or pedestrian accidents. In these cases, the $10,000 PIP limit is usually exhausted within the first hour of emergency room care. The "no-fault" label often serves as a shield for insurance companies to hide behind. It discourages victims from seeking the full compensation they deserve. We pierce through that shield to ensure accountability.

The Aggressive Tactics of Florida Insurers

Insurers in Boca Raton and Miami use sophisticated tactics to minimize payouts. They may offer a quick settlement check within days of the accident. If you accept this check, you are likely signing away your right to seek any further compensation. They hope you’ll take the bait before you realize the true extent of your injuries. They might also use your own recorded statements against you to deny coverage. This is why having a "Protective Champion" is essential. Steve Charles understands these games and counters them with relentless advocacy. We don’t accept lowball offers. We demand superlative outcomes for every client we represent.

Don’t let an insurance adjuster dictate the value of your recovery or your future. If you are struggling to get the compensation you need after a crash, you need a force that can fight back. Contact Steve Charles today to schedule a consultation and learn how we secure the financial restitution you are owed.

Why You Need Steve Charles to Navigate Florida’s Complex Laws

You now know the technical answer to is Florida a no fault state, but knowing the law is only half the battle. The other half is won through aggressive advocacy and a refusal to settle for less than you deserve. Steve Charles provides a formidable shield for the injured in Boca Raton, ensuring that insurance companies don’t trample your rights. We don’t just fill out forms. We launch a mission to secure the superlative outcomes necessary for your long-term recovery. If you want a dedicated ally who understands the high stakes of South Florida litigation, then our firm is your first call.

Our representation is built on a clear, risk-free foundation. If we do not win your case, then you do not pay us any legal fees. This "if-then" logic removes the financial burden from your shoulders, allowing you to focus entirely on your physical healing. While the $10,000 PIP cap is a hurdle for many, we view it as a starting point. We look beyond the minimums to identify every possible source of financial restitution. Whether it’s a negligent driver, a trucking corporation, or a rideshare entity, we pursue every avenue of liability with a confrontational spirit.

Trial-Ready Representation in Fort Lauderdale and Miami

Insurance adjusters in Miami and Fort Lauderdale know which lawyers settle and which lawyers fight. We prepare every single case as if it is heading to a jury trial. This trial-ready posture is the only way to force insurance companies to take your claim seriously. By handling the conflict on your behalf, we remove the anxiety of legal terminology and aggressive adjuster tactics. We are the expert advocates for the individual, providing the strength of a large firm with the personal care of a dedicated partner. Your recovery is our priority; our mission is your justice.

Take Action: Schedule Your Free Consultation Today

The first few hours after a crash are the most critical for your case. Evidence can be lost, and insurance companies will move quickly to limit their exposure. You need a team that operates with a rhythm of perpetual readiness. When you meet with Steve Charles, you get a direct assessment of your case and a clear path forward. There is no "slow" phase in our communication. We move rapidly from identifying your problem to implementing a solution. Contact Charles Injury Law now to protect your rights and ensure you have a Protective Champion in your corner.

Secure the Justice You Deserve After a Florida Crash

The technical reality of is Florida a no fault state does not have to be a barrier to your financial recovery. You now understand that PIP is only the first step and that the serious injury threshold provides a path to holding negligent drivers accountable in Miami and Fort Lauderdale. Don’t let the 14-day rule or insurance company tactics rob you of the restitution you deserve. If you have been injured, then you need a force that refuses to back down from a fight.

Steve Charles provides the aggressive advocacy and trial-ready representation required to secure superlative outcomes. We operate on a contingency basis; if we don’t win your case, then you don’t pay a single dime in legal fees. This risk-free approach ensures you can focus on your health while we handle the conflict. You have a limited window to take action under Florida law. Fight back against insurance denials; schedule your free consultation with Steve Charles today. Your future is worth the fight, and we are ready to lead the way.

Frequently Asked Questions

Is Florida a no-fault state for car accidents?

Can I sue for a car accident in Florida if it’s a no-fault state?

You can sue the at-fault driver if your injuries meet the "serious injury threshold" defined by Florida law. This includes permanent injuries, significant scarring, or the loss of a bodily function. If your case qualifies, you can bypass the PIP limits to seek full financial restitution for pain and suffering. Steve Charles aggressively pursues these claims to ensure insurance companies don’t hide behind the no-fault label to avoid paying what you are truly owed.

What does PIP mean in Florida insurance?

PIP stands for Personal Injury Protection, which is a mandatory insurance coverage for all Florida vehicle owners. It acts as an immediate financial shield by providing coverage for medical expenses and disability benefits without the need to prove fault. This system is designed to reduce the number of small claims in the court systems of Miami and Fort Lauderdale. It ensures that accident victims receive prompt medical attention during the most critical hours following a collision.

How much does PIP pay for medical bills in Florida?

PIP covers 80% of reasonable medical expenses and 60% of lost wages, up to a $10,000 limit. However, there’s a significant trap; you only get the full $10,000 if a doctor diagnoses you with an Emergency Medical Condition (EMC). If you don’t receive this specific diagnosis, your medical benefits are capped at just $2,500. We fight to ensure your medical records accurately reflect the severity of your condition so you don’t lose out on your rightful benefits.

What happens if my medical bills exceed the $10,000 PIP limit?

How long do I have to see a doctor after a car accident in Florida?

You have exactly 14 days from the date of the accident to seek initial medical treatment. If you wait 15 days, your insurance company will legally deny your PIP claim, and you will receive zero benefits. This rule is absolute and leaves no room for error. Even if you feel fine, you must get a professional evaluation immediately to preserve your right to financial recovery and ensure your health isn’t at risk.

Does no-fault insurance cover property damage to my car?

No, Florida’s no-fault system does not apply to property damage. The driver who caused the accident is still financially responsible for the damage to your vehicle. You will typically file a claim against the at-fault driver’s Property Damage Liability (PDL) insurance to cover your repair costs or the total value of your car. If the other driver is uninsured, then your own collision coverage may be your primary source of recovery for the vehicle.

Do I need a lawyer for a no-fault accident in Miami?

Yes, because the "no-fault" system is often used as a tool by insurers to minimize your payout. Insurance adjusters in Miami are trained to look for reasons to deny your claim or cap your benefits at the $2,500 non-emergency limit. A lawyer like Steve Charles acts as your expert advocate, handling the conflict so you can focus on recovery. If the insurance company refuses to play fair, then we are prepared to take them to court to secure a superlative outcome.

Disclaimer

The information provided on this blog is for general informational purposes only and does not constitute legal advice. Viewing this content does not create an attorney-client relationship with the firm. You should not act or rely on any information contained herein without seeking legal advice from a qualified attorney regarding your individual situation.