An insurance company lowball offer is not a final verdict on your claim; it’s a calculated test of your resolve. If you are currently struggling with rising medical bills in Fort Lauderdale, an adjuster’s quick settlement offer might feel like a lifeline, but it’s often a trap. They want you to sign before you realize the full extent of your injuries. When you receive an insurance company lowball offer what to do becomes the most important question for your financial recovery and your family’s future.

You might feel pressured to accept a small check because you worry your case isn’t "big enough" for a lawyer. We understand that pressure, but you shouldn’t let an insurance company dictate your worth. This guide provides the aggressive strategies you need to reject insulting offers and secure the maximum compensation you deserve under Florida law. If you stand your ground with Charles Injury Law, then you can shift the power back in your favor. We will preview the exact steps to take to ensure your medical bills and pain are fully covered by the settlement you actually earned.

Key Takeaways

- Learn how to identify when an initial settlement fails to cover your long-term medical needs and lost earning capacity under Florida law.

- Discover the specific strategies regarding an insurance company lowball offer what to do to ensure you do not leave money on the table.

- Understand why cashing a quick check often triggers a finality clause that prevents you from seeking more money for hidden injuries that appear weeks later.

- Find out how to formally reject an inadequate offer in writing to force the insurance adjuster to treat your claim with the respect it deserves.

- See how Charles Injury Law uses aggressive litigation tactics and deep discovery to secure the maximum compensation for our clients.

Table of Contents

Why Insurance Companies Send Lowball Offers in Florida

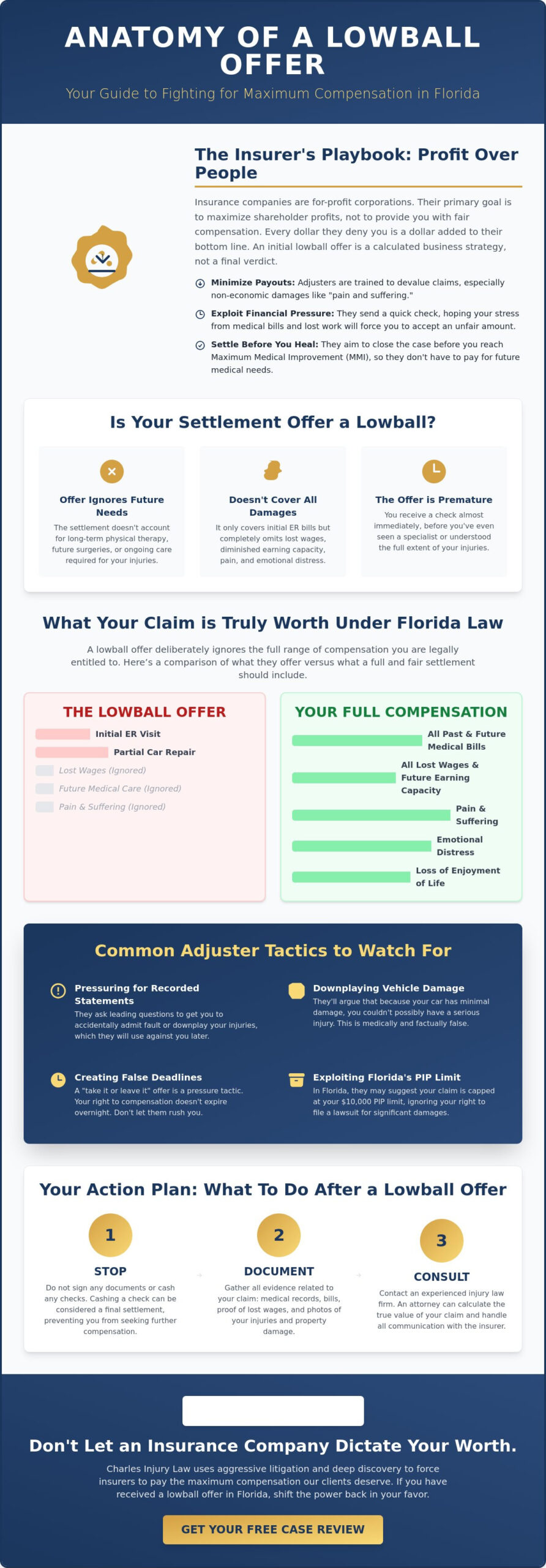

Insurance companies aren’t in the business of helping people. They’re in the business of keeping money. These are massive, for-profit corporations that prioritize shareholder dividends over the well-being of accident victims. If you are wondering about an insurance company lowball offer what to do, you must first understand their motivation. Every claim they pay reduces their quarterly profits. To an adjuster, your pain is just a line item they need to minimize. They use psychological tactics to make you feel like your case is weak, hoping you will accept pennies on the dollar.

The "First Offer" tactic is a classic move in the insurance industry playbook. They send a check almost immediately after a crash, sometimes before you’ve even seen a specialist. This exploits your financial stress. Between rising medical bills and time missed from work, many victims feel desperate. The insurer knows this. By offering a quick, low settlement, they hope you’ll sign away your rights before you realize the true cost of your recovery.

The Profit Motive vs. Your Recovery

Every dollar an insurer saves is a direct boost to their bottom line. Adjusters are specifically trained to devalue "pain and suffering" damages. These are non-economic losses that don’t have a fixed receipt, making them easy targets for lowballing. They often push for a settlement before you reach Maximum Medical Improvement (MMI). If you settle before your doctor determines you’ve recovered as much as possible, you lose the right to claim any future medical costs. This strategy often borders on a violation of the implied covenant of good faith and fair dealing that should govern every insurance contract in Florida.

Common Tactics Used in Miami and Fort Lauderdale

Adjusters in cities like Miami and Fort Lauderdale use specific pressure points to force quick signatures. You might encounter the "take it or leave it" deadline. This is almost always a false sense of urgency designed to trigger panic. They want you to believe the money will disappear if you don’t act now. It won’t. Other common tactics include:

-

Recorded Statements: They ask "innocent" questions to get you to admit to a pre-existing injury, which they then use to devalue your current claim.

-

Vehicle Damage Downplaying: If your car only has a minor dent, they argue it’s impossible for you to have a serious spinal injury.

-

PIP Exploitation: They use Florida’s $10,000 Personal Injury Protection (PIP) limit to suggest your case has no further value, ignoring your right to pursue a car accident lawsuit for significant damages.

If you see these red flags, don’t panic. An insurance company lowball offer what to do involves recognizing the game they are playing. At Charles Injury Law, we see through these corporate maneuvers. We know that a low offer is just the beginning of the fight, not the end of it.

How to Identify a Lowball Settlement Offer

A lowball offer is any settlement amount that fails to account for the full scope of your economic and non-economic damages. It is not a gesture of goodwill. It is a strategic attempt to close your file for the lowest possible price. If you receive an offer before your medical treatment is complete, it is a lowball by definition. The insurance company cannot possibly know your future needs while you are still in the middle of your recovery. Understanding navigating the insurance claims process helps you spot these predatory tactics before you sign away your rights.

The "General Damages" gap is where most victims lose the most money. Insurers often offer to pay for your initial emergency room visit while completely ignoring your physical pain and emotional distress. If you find yourself wondering about an insurance company lowball offer what to do, start by auditing your medical records against their offer. If the numbers don’t match your reality, the offer is an insult. You deserve a settlement that reflects the true impact the accident has had on your life.

Economic Damages in Florida

You must gather every invoice from your healthcare providers in Boca Raton or Palm Beach to establish a baseline for your claim. Don’t stop at current bills. You must also calculate lost wages, which include missed overtime and any promotional opportunities you lost due to your injuries. Florida law allows for the recovery of future medical expenses that are reasonably certain to be necessary for your continued care. If your injuries require long-term rehabilitation, a settlement that only covers the past is a failure. If you aren’t sure how to calculate these costs, you should reach out for a professional case review to protect your financial future.

Non-Economic Damages: The Hidden Value

Non-economic damages represent the human cost of an accident. This includes "loss of enjoyment of life," which quantifies the activities you can no longer perform, such as walking on the beach in Palm Beach or playing with your children. If you have suffered permanent scarring or disfigurement, Florida law permits you to seek significant compensation for that lasting impact. Insurers almost never include these figures in a first offer. They rely on your lack of legal knowledge to save themselves thousands of dollars. We don’t let them get away with it. Charles Injury Law identifies these hidden values and demands they be included in your final recovery.

Steps to Take When You Receive an Inadequate Offer

Do not sign anything. The moment you cash a settlement check or sign a release form, your case is over. Under Florida law, these documents typically contain a finality clause that prevents you from seeking further compensation, even if your injuries worsen later. If you are facing an insurance company lowball offer what to do involves a structured, aggressive response. You must pivot from a victim to a claimant who demands accountability. Understanding how the claim process works is vital, but remember that insurers often deviate from these standards to protect their own profits.

Formally reject the offer in writing. A verbal "no" over the phone leaves no paper trail. You must force the insurer to justify their valuation. Demand they explain exactly how they reached their figure and which medical records they chose to ignore. While you wait for their response, gather additional ammunition. Secure updated medical records from your specialists in Miami or Fort Lauderdale. Obtain expert witness statements or updated repair estimates from shops in Boca Raton. This evidence proves your claim is backed by reality, not just a desire for money.

Drafting a Formal Rejection

Your rejection letter must be a clinical, fact-based document. List every specific medical diagnosis the adjuster overlooked. If they ignored a herniated disc or signs of a traumatic brain injury, cite the specific medical report. Avoid emotional language. Stick to the evidence and relevant Florida statutes. End the letter by setting a clear, firm deadline for a revised response. This signals that you are in control of the timeline, not the insurance company.

The Power of a Counter-Offer

Set your counter-offer high. You need to leave room for negotiation while ensuring the final number reflects your true losses. We represent our clients by creating a comprehensive "demand package." This is a trial-ready file that includes all your medical evidence, wage loss documentation, and proof of liability. By explicitly mentioning personal injury litigation in your correspondence, you signal that you are prepared to take the fight to Florida courts. If the insurer sees you are ready for a legal battle, they are far more likely to increase their offer. Charles Injury Law stands ready to initiate this aggressive litigation if the insurance company refuses to act in good faith.

The Risks of Accepting a Quick Settlement Check

The allure of a fast check is powerful when bills are mounting in Fort Lauderdale. However, that check is a Trojan horse. Under Florida law, signing a release of liability is a terminal act for your legal case. It doesn’t just pay for your current bills; it waives your right to ever ask for another cent from that insurer. If you are questioning an insurance company lowball offer what to do, the answer is simple: do not cash it. Speed is the insurer’s greatest weapon against your long-term financial recovery.

Many victims fall into the "hidden injury" trap. Symptoms of a traumatic brain injury or chronic spinal issues often don’t peak until weeks after a car accident in Miami. If you settle before these symptoms manifest, you are personally responsible for every dollar of your future care. A $5,000 quick check might seem helpful now, but it is worthless if you later discover you need a $50,000 surgery. You’re effectively trading a jury-ready claim for a fraction of its true value.

Medical liens add another layer of danger. If your health insurance paid for your initial emergency care, they often have a legal right to be reimbursed from your settlement. If you accept a lowball offer, your entire settlement could go directly to your health insurance provider. This leaves you with zero dollars for your pain, suffering, or lost wages. This is why you must consult with a trial lawyer before you touch any settlement check.

Understanding the Release of Liability

A signed release in Florida is a binding contract that immediately terminates your right to sue the negligent party for that specific incident. Never trust an adjuster who claims they can "add more later" if your condition worsens. They won’t. They are legally protected once that document is signed. Settling before you reach a point of permanent impairment evaluation is a financial disaster. You are essentially gambling with your future health against a corporation that wants you to lose.

The Impact on Future Care

A quick settlement often leaves victims paying out-of-pocket for essential care months down the road. While Florida law requires $10,000 in Personal Injury Protection (PIP), this amount is rarely enough to cover major surgeries or long-term physical therapy. If you sign away your rights too soon, you lose the ability to hold the at-fault driver’s bodily injury coverage accountable. Don’t sign away your rights. Contact Charles Injury Law for a free case review before you agree to any terms.

How Charles Injury Law Forces Insurers to Pay

We don’t play by the insurance company’s rules. While many firms are content to "process" claims and accept the best offer they can get over the phone, we prepare every case for a jury. This trial-ready mindset changes the entire dynamic of the negotiation. If an adjuster realizes they are dealing with a firm that won’t hesitate to file a lawsuit in Florida courts, the value of their offer often increases overnight. When you are deciding on an insurance company lowball offer what to do, choosing a firm with a reputation for litigation is your strongest move.

Our strategy relies on aggressive discovery. We don’t just take the adjuster’s word for why they devalued your claim. We demand their internal notes and the valuation data they used to generate their offer. If they used biased software or ignored specific medical evidence, we expose those flaws. We also deploy a sophisticated network of experts in Miami and across Florida. This includes accident reconstructionists who prove liability and medical experts who testify to the long-term impact of your injuries. We build a wall of evidence that corporate bullies cannot ignore.

We also leverage Florida Bad Faith statutes to hold insurers accountable. Florida law requires insurance companies to act fairly and honestly toward their policyholders and claimants. If an insurer uses deceptive tactics or refuses to settle when they should, we pursue every available legal avenue to punish that behavior. This confrontational spirit ensures that the insurer remains focused on their financial exposure if they continue to lowball your claim.

Our Trial-Ready Approach

Insurance companies maintain databases on law firms. They know which attorneys are afraid of the courtroom and which ones are ready to fight. Charles Injury Law acts as your Protective Champion. We shield you from the stress of the conflict while we handle the heavy lifting of litigation. Our reputation for excellence extends to complex cases, including truck accidents in Florida, where the stakes are highest and the insurers are most aggressive. If the insurer won’t pay what is fair, then we will see them in court.

No Fees Unless We Win

We’ve removed the financial barriers to elite legal representation. We work on a contingency fee basis, which means you don’t pay us a single cent unless we successfully recover money for you. This aligns our interests perfectly with yours. We are fully committed to securing the maximum compensation for victims in Boca Raton and Fort Lauderdale. You shouldn’t have to worry about legal bills while you’re trying to heal from an injury. If you’re ready to stop being a victim of corporate greed, you can fight back against lowball offers today by initiating your case with a team that knows how to win.

Demand the Accountability You Deserve

A lowball offer is a psychological tactic, not a final decision. You now have the tools to identify these predatory settlements and the steps to reject them effectively. If you refuse to be intimidated, then you can secure a future that covers every medical bill and lost wage. We treat every client as a priority and every case as a mission for justice. Charles Injury Law stands as a formidable shield for victims in Miami and Fort Lauderdale.

Understanding an insurance company lowball offer what to do is the first step toward reclaiming your life. Our firm provides aggressive advocacy against major insurance carriers to ensure they pay every dollar you are owed. We offer trial-ready representation focused on maximum recovery. Our no-fee guarantee ensures you pay nothing unless we win your case. You’ve suffered enough; let us handle the conflict while you focus on your recovery. We are ready to fight for the superlative outcome your family needs.

Secure the Maximum Compensation You Deserve—Contact Charles Injury Law Now

Frequently Asked Questions

How do I know if the insurance company’s offer is a lowball?

An offer is a lowball if it fails to cover your total medical bills, lost wages, and future care needs. If an adjuster calls you within days of a crash in Miami, the offer is almost certainly inadequate. They are guessing at your recovery time before you’ve even finished treatment. If you receive an insurance company lowball offer what to do is compare it against your actual invoices. If the math doesn’t protect your family’s future, it’s an insult.

Can I negotiate a settlement offer on my own in Florida?

You can attempt to negotiate alone, but you are at a massive disadvantage. Insurance adjusters are professional negotiators backed by corporate legal teams. They use specific tactics to minimize your pain and suffering. If you represent yourself, they may never offer the true value of your claim. Charles Injury Law levels the playing field by using aggressive litigation strategies to force higher settlements for victims in Fort Lauderdale.

What happens if I already cashed the insurance check?

If you cashed the check, your case is likely over. Most insurance checks in Florida come with a release of liability clause. Cashing the check usually signals your legal acceptance of the final settlement. This bars you from seeking more money even if your injuries get worse. If you haven’t cashed it yet, stop immediately. You need a professional review to ensure you aren’t signing away your rights for pennies.

How much does a personal injury lawyer cost in Fort Lauderdale?

You pay nothing upfront for our services. We work on a contingency fee basis. This means we only get paid if we successfully recover money for your case. If we don’t win, you don’t owe us a dime. This risk-free structure allows victims in Fort Lauderdale to access elite legal advocacy without worrying about hourly rates. Our goal is to remove the financial burden while we fight for your recovery.

What is the average settlement for a car accident in Florida?

There is no true "average" because every injury is unique. Your settlement depends on your medical bills, the severity of your injuries, and the available insurance policy limits. A minor fender-bender results in a different recovery than a catastrophic crash. We focus on securing the maximum compensation for your specific losses. We look at everything from current surgery costs to your lost earning capacity in Palm Beach.

How long do I have to respond to an insurance settlement offer?

Florida law doesn’t set a specific deadline for responding to a private offer, but the statute of limitations for negligence is generally two years. Adjusters often use fake deadlines to pressure you. They want you to panic and sign quickly. If you’re stressed about an insurance company lowball offer what to do, don’t let them rush you. Take the time to consult with an expert who can evaluate the offer’s fairness.

Will my case have to go to court if I reject a lowball offer?

Most cases settle before a trial begins. However, we treat every case as if it is going to court. This aggressive preparation often forces the insurer to settle for a fair amount to avoid the risks of a jury verdict. If the insurance company refuses to pay what you deserve, then we are ready to fight for you in Florida courts. Our reputation for litigation is your greatest leverage during negotiations.

Does Florida law require me to accept the first offer?

No, you are never legally required to accept any settlement offer. The first offer is simply a starting point for negotiations. You have the right to reject it and demand a figure that reflects your true damages. If the insurer acts in bad faith during this process, Florida statutes provide pathways to hold them accountable. You have the power to say no and fight for a superlative outcome for your case.

Disclaimer

The information provided on this blog is for general informational purposes only and does not constitute legal advice. Viewing this content does not create an attorney-client relationship with the firm. You should not act or rely on any information contained herein without seeking legal advice from a qualified attorney regarding your individual situation.